Ever stood at the pharmacy counter and felt a surge of panic when the pharmacist told you your medication would cost $85 instead of the $10 you expected? You aren't alone. Millions of people run into this wall every year because of the complex way insurance formularies is a list of prescription drugs covered by a health insurance plan, organized into tiers to determine the cost-sharing for the patient. The difference between getting a brand-name drug and its generic version isn't just about the label on the bottle; it's about a set of rigid policies that decide how much of your paycheck goes toward your health.

| Feature | Generic Drugs | Brand-Name Drugs |

|---|---|---|

| Typical Formulary Tier | Tier 1 (Lowest Cost) | Tier 2 or 3 (Higher Cost) |

| Average Copay | $5 - $15 | $40 - $100+ |

| Prior Authorization Rate | Very Low (~2.1%) | Moderate to High (~22.7%) |

| Substitution Rule | Default choice for insurers | Requires "Dispense as Written" (DAW) |

The Financial Gap: Why Your Insurance Prefers Generics

From an insurance company's perspective, Generic Drugs are the gold standard for cost containment. These medications are chemical copies of original drugs, and the FDA requires them to have the same active ingredients, strength, and efficacy. Because generic makers don't have to spend billions on the initial research and development, they can sell the drug for significantly less. In fact, generics often cost patients 80% to 85% less than the branded versions.

To push patients toward these cheaper options, insurers use a tiered system. If you're on a Tier 1 plan, your generic might cost you a few dollars. But if you insist on the brand name, you might trigger a "brand-generic cost difference" clause. This means you don't just pay a higher copay; you pay the generic copay plus the entire price difference between the two products. It's a powerful financial nudge that makes brand names prohibitively expensive for most people.

Navigating the Substitution Maze

Most of the time, the choice between a brand and a generic isn't even yours to make-it's a policy decision. In almost every state, pharmacists are encouraged or required to substitute a generic if one is available. The only way to bypass this is if your doctor writes "Dispense as Written" (DAW) on your prescription. However, doing this doesn't guarantee the insurance company will pay for it; it only tells the pharmacist not to swap it.

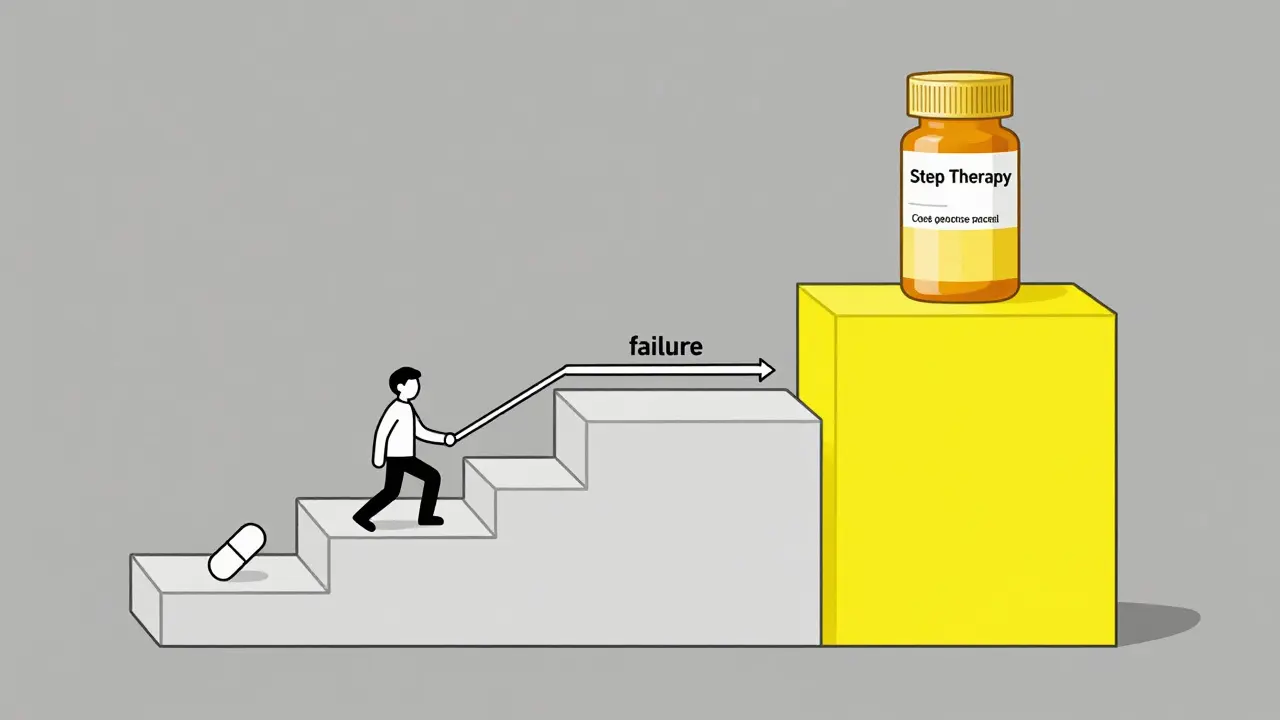

For those on Medicare Part D, the rules are even stricter. About 91% of these prescriptions are generics because the program mandates substitution unless it's medically necessary. If you find yourself needing the brand name for a medical reason, you'll likely encounter Step Therapy. This is a policy where the insurer forces you to "fail" on a generic version first-meaning you have to try it and prove it doesn't work-before they will agree to cover the more expensive brand-name alternative. This process can delay your actual treatment by six to eight weeks.

When "Same" Isn't Actually the Same

While the FDA insists that generics are therapeutically equivalent, real-world experience tells a different story for some. Many patients report different side effects or a lack of efficacy when switching. This often happens because of the inactive ingredients-the fillers and binders that aren't the active drug but affect how your body absorbs it. This is particularly common with thyroid medications or certain antiepileptics, where even a tiny variation in absorption can lead to therapeutic failure.

Because of this, some policies allow for "medical necessity exceptions." If you have a documented adverse reaction to a generic, your doctor can file for an exception. However, this isn't a smooth process. You may need to provide specific documentation codes, like the 'YN1' modifier used by CMS, to prove why the brand name is required. In some states, like California, laws are more protective, requiring insurers to cover the brand name if a generic causes a bad reaction. In others, like Texas, the rules are much tighter, limiting brand coverage only to cases where no equivalent exists at all.

The Role of PBMs and Prior Authorizations

Behind the scenes, Pharmacy Benefit Managers (or PBMs) are the ones actually writing the rules. PBMs negotiate prices with drug makers and decide which drugs make the "preferred" list. They use Prior Authorization as a gatekeeping tool. While only about 2% of generics require this, nearly 23% of brand-name drugs do. This means your doctor has to jump through hoops, submitting forms and waiting days or weeks for approval before you can even pick up your medicine.

Interestingly, we are seeing the rise of "authorized generics." This is when the original brand-name company decides to sell its own version of the drug as a generic. These often get better coverage and more trust from insurers than third-party generics, creating a strange middle ground in the pharmaceutical market.

Dealing with the "Donut Hole" and Costs

For Medicare users, the coverage gap-famously known as the "donut hole"-adds another layer of stress. Once you spend a certain amount on drugs, there's a period where you are responsible for a larger portion of the cost. While the Inflation Reduction Act of 2022 has started to cap out-of-pocket spending, the difference between a generic and a brand name in this gap can be the difference between affording your meds and skipping doses.

If you're struggling with brand-name costs and have commercial insurance, you might look into manufacturer copay cards. These can sometimes drop your cost to nearly zero. But be careful: federal law prohibits these cards for Medicare and Medicaid beneficiaries to prevent manufacturers from influencing the government's drug spending.

Will my insurance cover a brand-name drug if the generic makes me sick?

Yes, but it usually requires a "medical necessity exception." Your doctor must document the adverse reaction and submit a request to your insurer. Some states have laws that mandate this coverage, but it typically involves a prior authorization process that can take several business days.

What is "Step Therapy" in insurance policies?

Step therapy is a requirement that you try a lower-cost medication (usually a generic) before the insurance company will agree to pay for a more expensive brand-name version. If the generic is ineffective or causes side effects, you "step up" to the brand-name drug.

Why do some generics feel different even if the active ingredient is the same?

While the active ingredient is identical, the inactive ingredients (fillers, binders, and dyes) can vary. These can affect how the drug is absorbed by your body, which is why some people experience different side effects or efficacy with different generic manufacturers.

What does "Dispense as Written" (DAW) mean?

DAW is a notation a doctor puts on a prescription to tell the pharmacist not to substitute the brand-name drug with a generic. While this ensures you get the brand, it does not guarantee your insurance will cover the cost; you may still have to pay the brand-name copay or the full price difference.

Are there any drugs that are always covered as brands?

Some "narrow therapeutic index" drugs (like warfarin or phenytoin) have more flexible policies because small changes in dosage or absorption can be dangerous. In about 27 states, these may be covered as brands without as much documentation.

Next Steps for Patients

If you're facing a sudden spike in medication costs, your first move should be to check your plan's formulary. Look for where your drug sits-Tier 1, 2, or 3. If you're being forced onto a generic that isn't working, don't just suffer through it. Schedule a visit with your doctor specifically to discuss a "medical necessity" appeal. Bring a log of your symptoms and the specific generic manufacturer's name from the bottle, as this helps the insurer understand exactly which version caused the issue.

Stephen Luce

It's honestly heartbreaking how many people have to choose between their rent and their medication because of these tiered systems. I've seen so many friends struggle with the stress of not knowing if they can actually afford their prescription until they get to the window. The whole process is just overwhelming for someone who's already sick.

Srikanth Makineni

pbm system is a joke

Timothy Burroughs

this is why the us is the only place where people actually go broke over a pill bottle it's absolute madness that we let these pbm vultures decide who lives and who dies based on a tier list’s budget just disgusting

Daniel Trezub

Actually, the whole 'inactive ingredients' argument is mostly a placebo effect for the vast majority of people. I mean, sure, it's true for a tiny fraction of narrow-index drugs, but for most things, it's just people wanting to feel like they're getting a premium product. The FDA standards are plenty strict enough that the a-b-c of the pill doesn't change the chemistry of the result. Most people just like the prestige of the brand name and then complain about the price.

Alexander Idle

Oh for the love of everything, this whole explanation is just an absolute tragedy of bureaucracy! It is truly a Shakespearean drama that we must first 'fail' a medication like some sort of clinical experiment before the corporate overlords grant us the privilege of actual health. Truly, the audacity of step therapy is simply breathtaking in its cruelty!

Christopher Cooper

I think it's worth mentioning that some patients can request a specific generic manufacturer if they've found one that works better than others. While the pharmacy might not always have every brand in stock, sometimes the 'authorized generics' mentioned here are the best of both worlds since they're made by the same company that developed the original drug. It's a great way to keep costs down while maintaining a level of quality you trust.

Dhriti Chhabra

It would be most beneficial if insurance providers offered more transparency regarding their formularies. The current complexity of the tiered system often leads to significant distress for the patient, and a more streamlined communication process would surely alleviate much of this burden for all parties involved.

Rupert McKelvie

Keep fighting those appeals! It takes a bit of patience and some paperwork, but once you get that medical necessity exception approved, it's a huge weight off your shoulders. There are always ways to get the right care if you keep pushing through the red tape.

Sarabjeet Singh

Just stay patient with the process. It's a grind, but getting the right meds is the only thing that matters in the end. Keep your head up.